nazarethman

Micron Technology, Inc. (NASDAQ:MU) has been a compelling investment opportunity over the past few years as it benefited from a number of coinciding trends. From acceleration of cloud computing and chip shortages, to strong memory demand for mobile devices and graphics products.

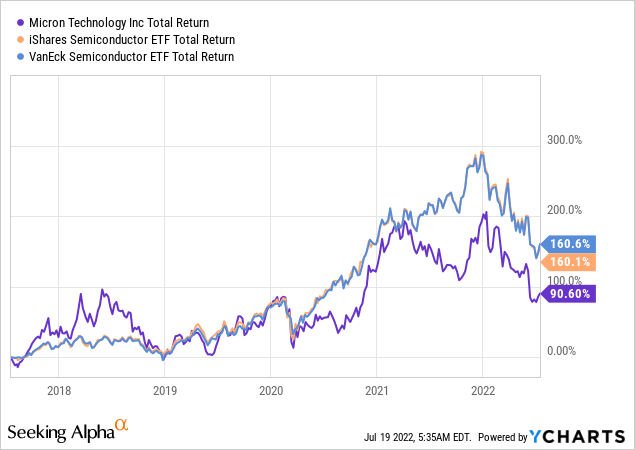

However, even as the company’s memory and storage products were riding on the wave of digitalization, Micron still underperformed the semiconductors sector as a whole.

To an extent, Micron’s performance should be compared to those of Samsung and SK Hynix since they are two direct peers in the memory and storage space. However, focusing entirely on this sub-segment of semiconductors would have resulted in far inferior returns over time. Therefore, throughout this article I will use an expanded peer group of large publicly traded semiconductors stocks.

Having said all that, Micron’s shareholders recently got some good news following the company’s announcement of a quarterly dividend.

Seeking Alpha

Not only that, but the dividend also saw a significant increase recently which sparked hopes of the stock turning into a strong dividend play on top of the high growth potential.

Micron Technology Investor Presentation

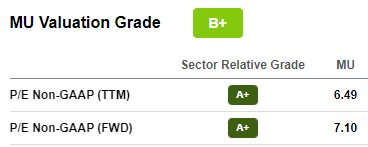

Last but not least, the company’s low multiples have made the investment proposition even more compelling by giving it significant margin of safety.

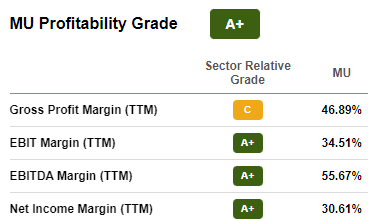

Micron’s Compelling Fundamentals

On the surface, it sounds as too good to be true. Micron currently has a dividend yield of nearly 1%, with the annual payments growing at a rate of 15%.

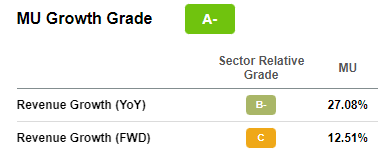

At the same time, the company’s topline continues to grow at double digit rates, while margins are at their highest levels both historically and against the sector averages.

Seeking Alpha Seeking Alpha

Last but not least, MU trades at multiples that one cannot find anywhere else in the large cap semiconductors space. Taking the Non-GAAP P/E ratio as an example, MU now trades at 7 times next year earnings (see below).

Seeking Alpha

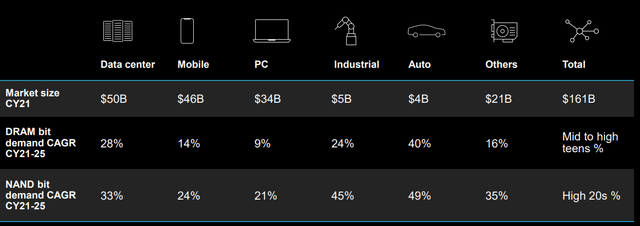

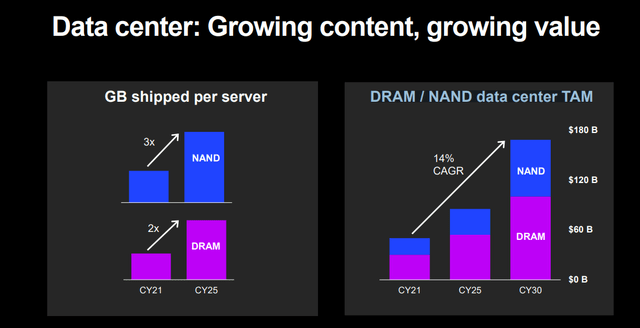

The narrative around future market size for both memory and storage solutions only sweetens the deal even more as demand from data center, industrial and automotive sectors is expected to grow at rates of above 20% on an annual basis.

Micron Technology Investor Presentation

In a nutshell, on the surface Micron appears as once in a lifetime opportunity – a high growth and profitable business that also trades at ridiculously low multiples and offers a growing dividend. However, as we dig deeper into Micron’s business model and take into account the highly cyclical nature of the business, Micron’s low multiples seem justified. Moreover, the current dividend is not something that long-term investors should count on.

What Should Investors Know About Micron Technology’s Business?

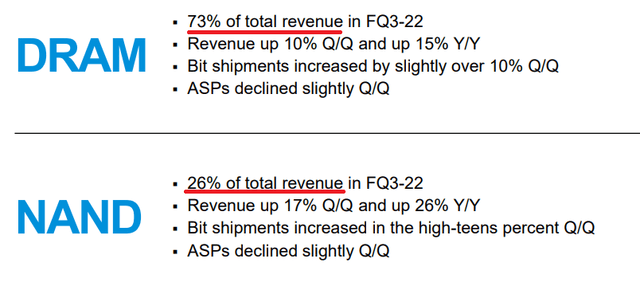

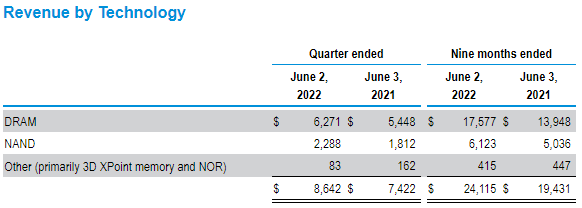

It is hardly a secret that in terms of revenue, DRAM makes roughly three-quarters of Micron’s business.

Micron Technology Investor Presentation

However, the footprint of DRAM is even larger on the company’s overall valuation. The reason for that is future expected growth on one hand and profitability (or return on capital more broadly) on the other. To begin with, for the past 9-month period NAND storage related revenues were roughly $6.1bn.

Micron Technology 10-Q SEC Filing

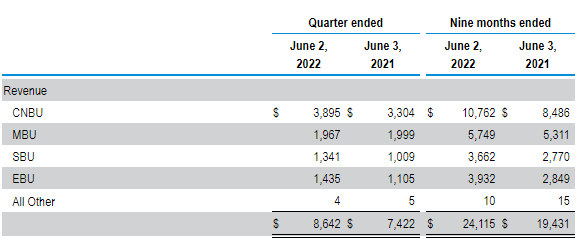

The SBU segment (Storage Business Unit) is roughly half of that number (see below) which leaves about $2.5bn worth of NAND sales for the MBU (Mobile Business Unit) and EBU (Embedded Business Unit). The CNBU (Compute and Networking Business Unit), on the other hand, includes only memory related products.

Micron Technology 10-Q SEC Filing

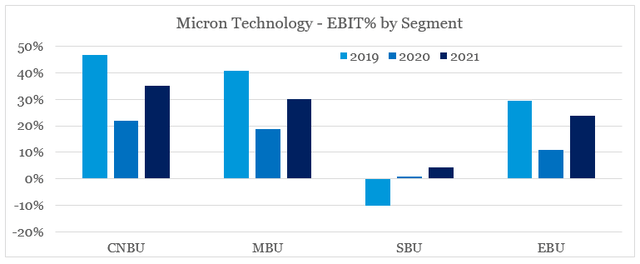

Having said that, the SBU is now barely profitable with significant losses prior to the elevated demand following the pandemic. The rest of the business units are selling primarily memory solutions and as such are the major profit drivers for Micron.

prepared by the author, using data from SEC Filings

Therefore, it is reasonable to conclude that DRAM is far more important for MU’s overall valuation and future returns. However, demand for DRAM solutions is also more volatile when compared to storage and Micron has little pricing power in a market that is dominated by the two South Korean giants – Samsung and SK Hynix.

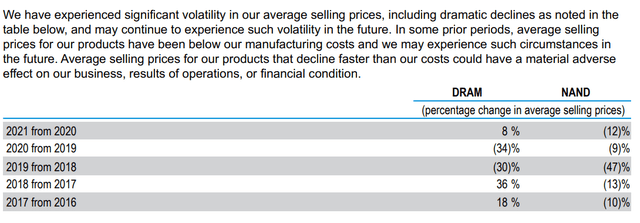

All that is clearly illustrated in the company’s annual report, under the risks section, where volatility in selling prices is noted as a major risk.

Micron Technology 10-K SEC Filing

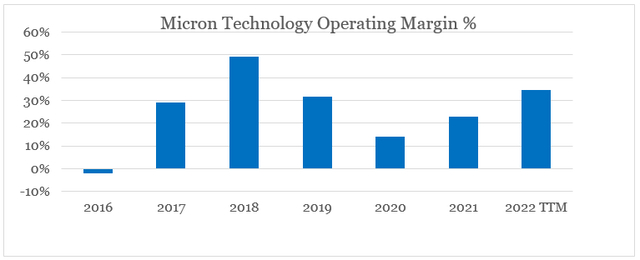

The impact of the change in DRAM average selling prices on Micron’s margins is also evident when we reconcile the table above with the graph below. During 2019 and 2020, averages selling prices of DRAM declined by 30% and 34% respectively and as a result MU operating margin fell from nearly 50% in 2018 to as low as 14% in 2020.

prepared by the author, using data from SEC Filings

Therefore, as exciting as the narrative for the future might sound, the reality is that slight variances in overall demand and average selling prices of DRAM could have profound implications for Micron’s profitability.

Micron Technology Investor Presentation

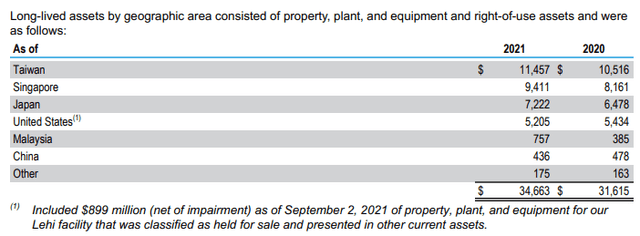

Last but not least, investors should not forget the political risk involved with the geographical positioning of Micron’s long-lived assets.

Micron Technology 10-K SEC Filing

The Earnings Variance

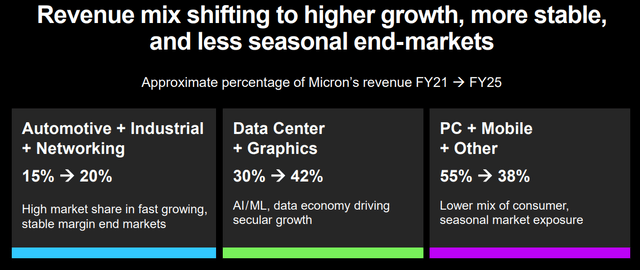

By far the largest risk for Micron’s shareholders and the recently initiated dividend payments is the highly cyclical nature of the industry and the commoditized nature of memory and storage products. Although the management has recently stressed the fact that certain end markets for the company’s products are more stable, Micron’s earnings remain highly cyclical.

Micron Technology Investor Presentation

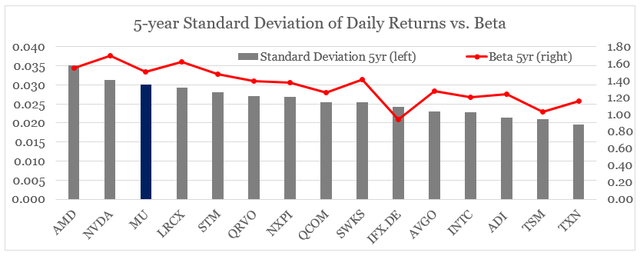

Just looking at the share price variance and the overall market exposure through the beta coefficient, Micron comes near the very top within its expanded peer group (see below).

prepared by the author, using data from Seeking Alpha

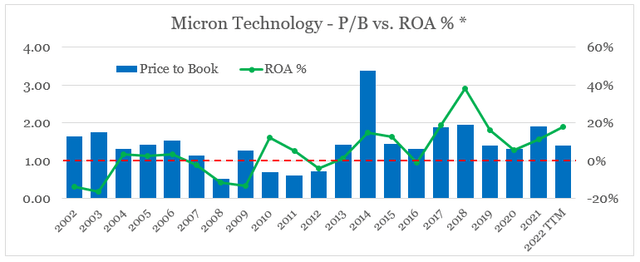

Cyclicality is also one of the main reasons why Micron rarely trades at more than twice its book value of equity, even though return on assets has improved significantly in recent years.

prepared by the author, using data from SEC Filings

* based on operating profit and total assets

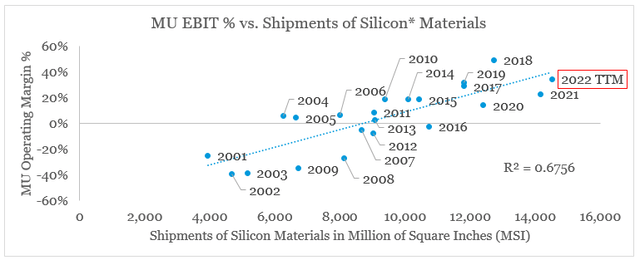

Moreover, MU’s margins are highly dependent on global demand and shipments of silicon materials. As the industry is highly capital intensive and cyclical in nature, manufacturers are often being capacity constrained during periods of elevated demand. This in turn provides a significant tailwind on pricing and consequently on margins. Investors, however, should not forget that the opposite is also true and margins could deteriorate quickly even in an event of a slight cool off in demand.

prepared by the author, using data from SEC Filings and semi.org

That is why simply extrapolating very recent trends into the future could lead to disastrous results.

Micron Technology Investor Presentation

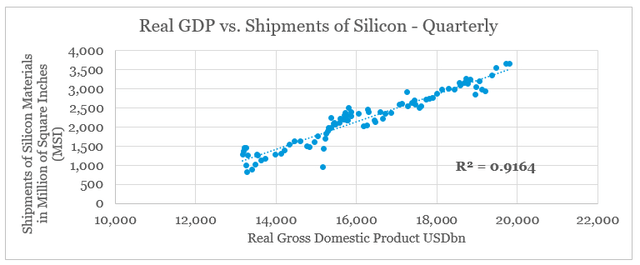

Although semiconductors are now part of every single aspect of our daily lives, the demand remains closely related to changes in real GDP numbers.

prepared by the author, using data from FRED and semi.org

* from Q1 2000 to Q4 2022

Having said all that, Micron’s earnings in the coming years will remain volatile no matter what the current narrative is. Of course, a global recession and demand slowdown are far from certain, however, investors should not expect Micron’s earnings volatility to disappear. Therefore, even as the roughly $500m annual dividend payments are well-covered by the company’s free cash flow for the moment, long-term investors should not count on consistent long-term dividend growth. Quite the opposite, the dividend is likely to be suspended indefinitely during the next business cycle downturn.

Conclusion

Micron Technology is without a doubt one of the leaders in both volatile and non-volatile memory. As digitalization trends accelerated in recent years and demand for DRAM skyrocketed, the capacity constrained industry enjoyed both volume and price increases. However, given the capital intensity and the highly cyclical nature of the industry, profit margins are at significant risk over the coming years. That is why the current low multiples are likely justified as they take into account all the risks associated with a potential business cycle downturn. Lastly, Micron’s dividend payments are unlikely to grow consistently beyond the short-term and the recently announced 15% increase is not indicative of the future.